Redefining round names, stretched fundraising timelines, and what’s on the horizon for technical investing

As I noted in this year’s YC batch recap, it’s no secret that AI is the common thread connecting most startups in 2025—and that trend isn’t slowing down. One stat that caught my attention: nearly a quarter of the current YC cohort have codebases that are almost entirely AI-generated.

What that stat misses, though, is key: these are technical founders using AI as leverage, not as a replacement for real engineering talent.

The meteoric rise of the AI-enabled developer

At Vermilion, we back technical founders building technical products, and increasingly, those products are for the AI-enabled developer—a developer whose workflow, team, and go-to-market are being reshaped by modern tooling, machine learning, and automation.

But what does this perspective mean when looking at the investment landscape right now and how it intersects with startups building technical tools for technical audiences?

The new normal: Series A is the new Seed is the new Pre-Seed

The funding stack is shifting fast. The strongest founders building at the intersection of developer and AI are skipping pre-seed entirely and going straight to seed—because they need more time and stability in their runway and they know the bar for a Series A is higher than ever.

Seed valuations are following suit. Just 18 months ago, we saw standard AI/infra/tech seeds land around $16M. Now, $20–25M is becoming the new floor. Some of that’s hype. Some of it is inflation. But most of it is a recognition that:

These are real companies with early traction and some great marquee brand name users.

The cost of doing business in AI (infra, talent, compute) isn’t cheap.

The runway needs to last ~2 years.

And the data agrees. Taking a look at Peter Walker, Head of Insights @ Carta’s VC fund performance for Q4 2024, a few things really stuck out to me aside from the fund performance metrics. I really recommend looking at the entire report and subscribing to Peter’s newsletter.

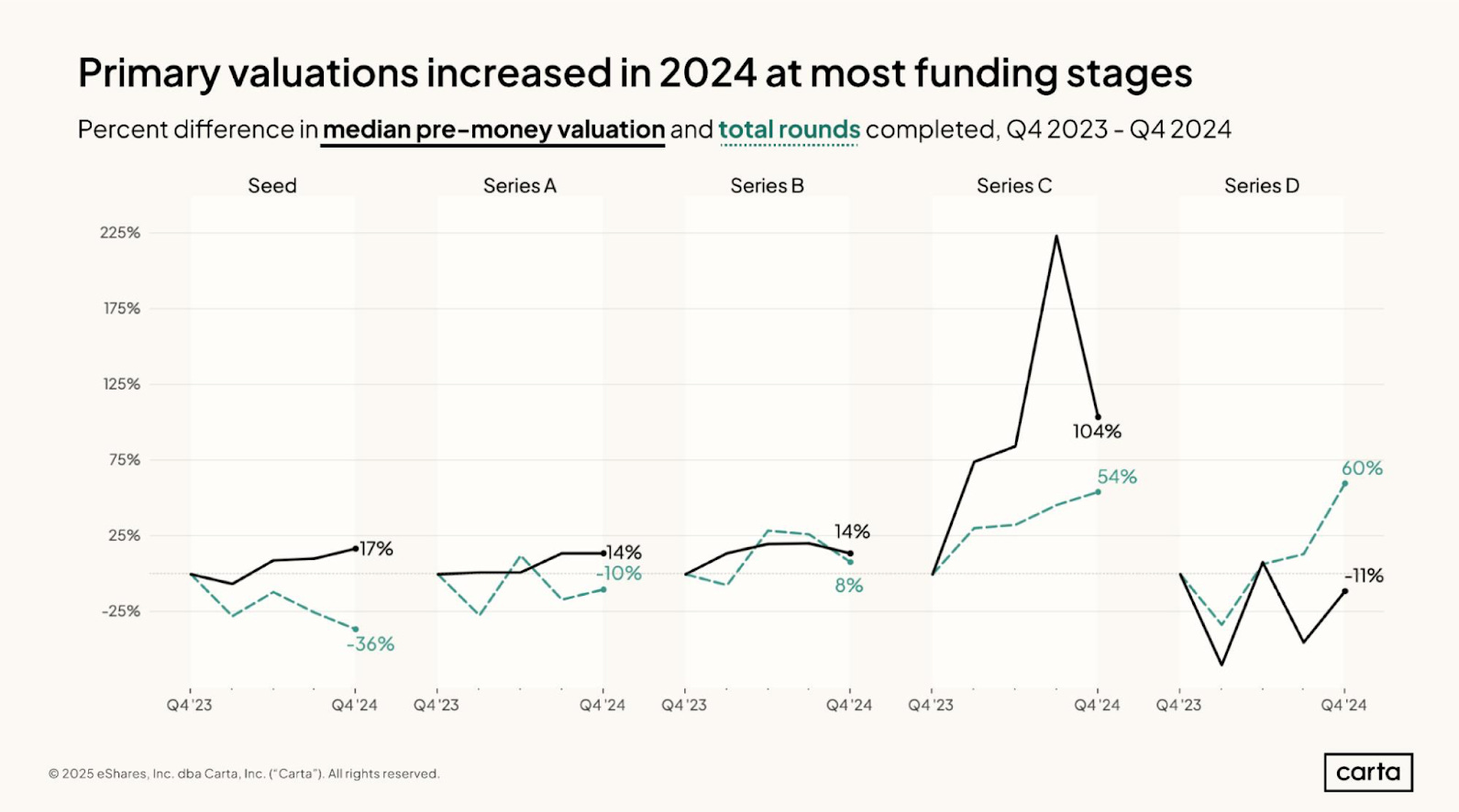

As we’ve seen in the market, round valuations at the earlier stages are going up. Seed round valuations pre-money have increased 17% year over year from Q4 2023 to Q4 2024. The total number of rounds at seed have decreased dramatically at 36% year over year. Prices are going up, companies getting funded are going down.

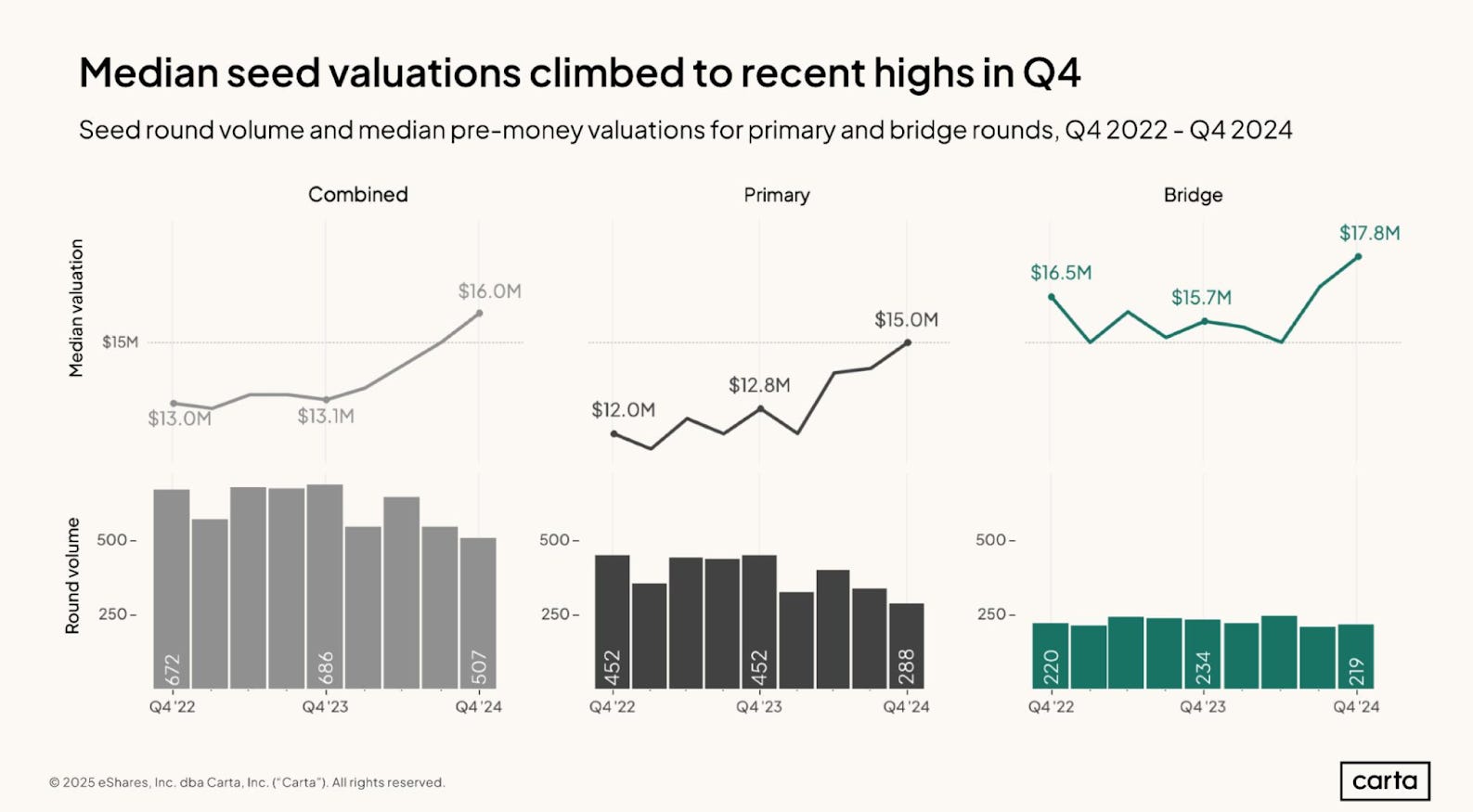

Dollar for dollar that looks like $16M for pre-money valuations at seed across all industries up from $13.1M just a year prior. I think if we went deeper in the data to industry level, technical product rounds would be the higher prices helping drive that median up. Combining primary funds raised with the rise of the seed bridge round, which are very common in this market, prices are higher than ever.

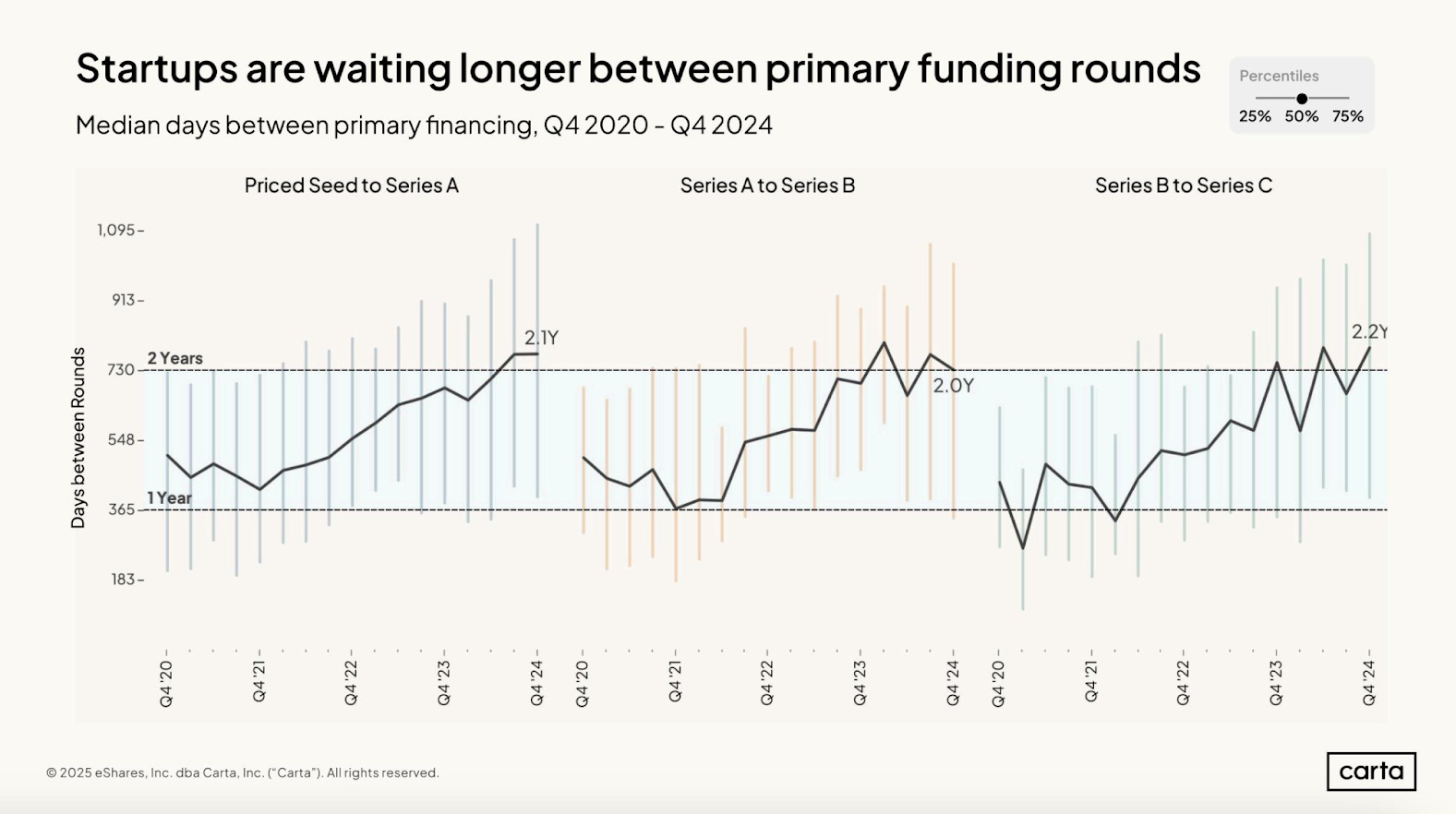

Founders are extending their time to series A because time between rounds is also increasing.

Why founders are stretching their runway

One of the biggest shifts we’re seeing is how long founders are waiting between primary rounds. In 2020, the average time between Seed and Series A was just over a year. In 2025, it’s more than 2.1 years.

That’s not just about macro uncertainty—it’s strategic. Today’s founders know:

Series A rounds require more maturity: Investors want revenue growth, real usage, and signs of product-market fit. A compelling narrative isn’t enough.

Big seeds = longer timelines: With $2M–$4M seed rounds becoming common, there’s more pressure to show outcomes before coming back to market.

Fundraising is harder: Fewer total deals are getting done, and the bar has gone up across the board.

AI tooling needs time to evolve: Some products require longer cycles to harden infra, prove use cases, and move from “cool demo” to sticky workflow. We always hear about long sales cycles in enterprise software but this is a longer product life cycle.

Founders are raising bigger early rounds, and treating them like they need to last. The “raise every 12 months” treadmill is slowing down—and that’s a healthy recalibration. Fundraising is stressful and takes so much time.

On the one hand, you don’t want to over value and over raise then make a series A impossible but you also don’t want to under capitalize your startup. It’s a balance that is very hard to get right. It mirrors raising a fund while there are so many moving pieces and needing to plan for 2.5 to 3 years in advance.

Exit optionality: Secondaries + green shoots

We’re still early in the fund cycle, but the secondary market is heating up. Founders, early employees, and early-stage funds are seeing more options to lock in partial liquidity. Add to that a slight uptick in M&A, and we’re optimistic about the next few years. While our exit landscape for this fund isn’t for another 10 years, at least, the current economics affect our founders raising their next round and what valuations they get locked into so we are all watching the exit landscape closely.

No one’s predicting a 2021-style IPO window reopening. But there’s real movement again—and real buyers—for companies showing strong monetization.

So… is it a Bubble?

Probably. Maybe. Depends what you mean. Everything is a bubble or a hype cycle in some way.

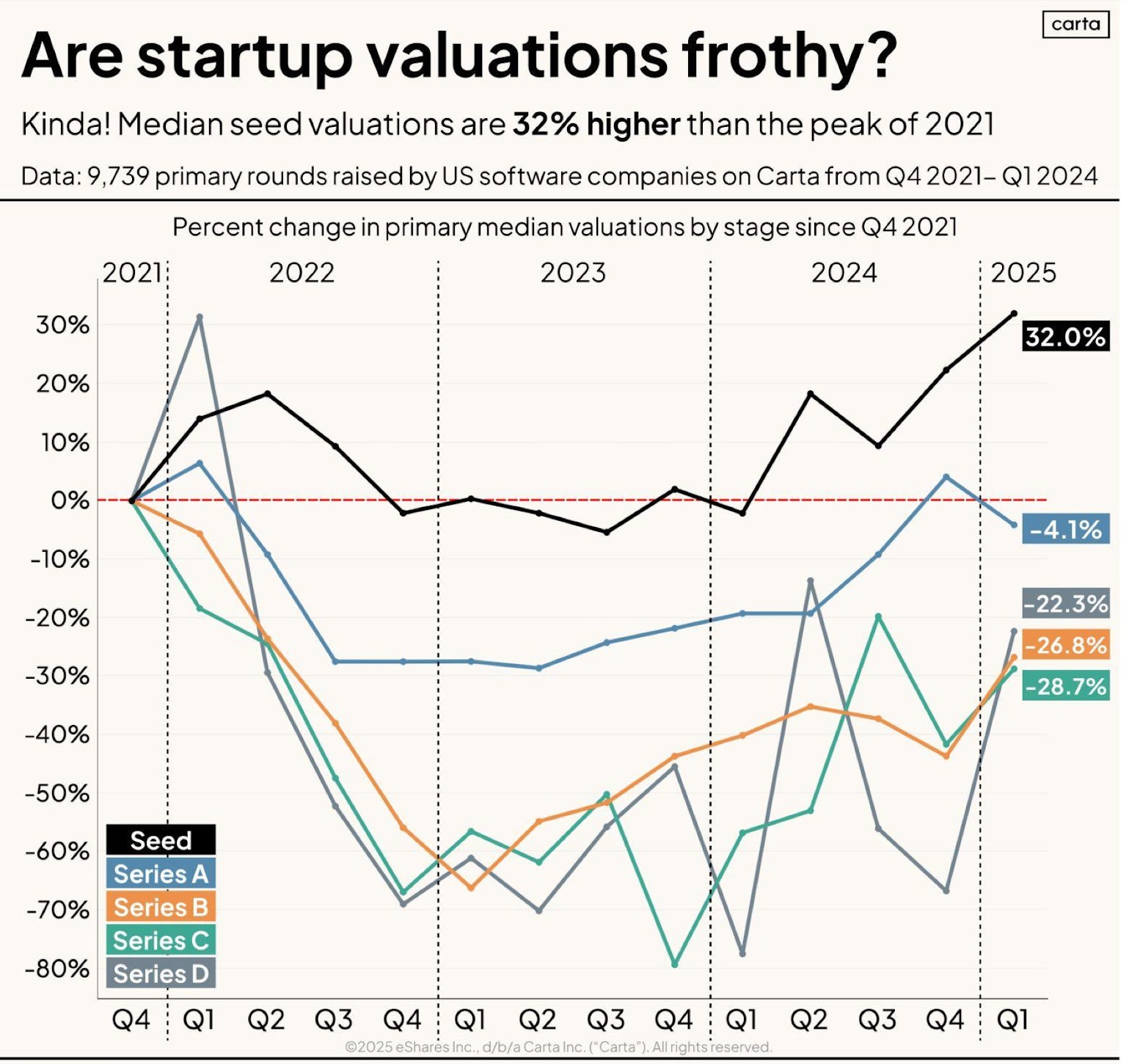

If you look at the most recent Q1 data, valuations are way up YoY for seed deals, round counts are still down, and capital is concentrating around breakout teams. I don’t think I’d use ‘frothy’ to describe…anything ever…but if you said slightly lofty but likely driven by a trend in actualization - sure.

We’re also seeing real product velocity, real revenue, and real customer pull. In short, category-defining products are being built right now—and they’re being built by technical founders with clear plans to monetize. It’s such an exciting time in early stage investing and company building.

The AI-enabled developer isn’t just a persona—it’s the center of a new wave of infrastructure and workflow innovation. That’s not a bubble. That’s a platform shift.

What we’re watching at Vermilion

Here are a few things we’re keeping a close eye on:

Valuation pressure: How long can the $25M seed hold? Is it sustainable without revenue? Do we raise more capital for the next fund in anticipation of that trend continuing?

Fundraising timelines: The average time from Seed to A is now 2.1 years—founders need enough capital to show real revenue growth before they raise again.

Geography trends: SF and NY are still where most breakout companies are clustering, even with remote teams - but don’t overlook the power of founders based between the coasts. Over the last few years geography for fundraising spread out quite a bit but for North America, we’re seeing dollars start to concentrate around SF and NY again. We’re seeing that re-concentration be mirrored in the public markets and later stage startups with RTO continuing to gain traction.

AI-native categories: Developer tools, security, data, infra—AI is in everything, and if it’s not, it’s probably getting leapfrogged. The tools we all loved just 10 years ago are being forced to fully rebuild their products and platforms to keep up in this market. It’s hard to watch some of my favorite companies from the 2010’s become legacy software but I suppose that’s what starts to happen when you’ve been in tech for long enough.

We’re excited about this moment. There's noise, sure—but there's also signal. And in that signal, we’re seeing the beginnings of the next generation of enduring technical companies.